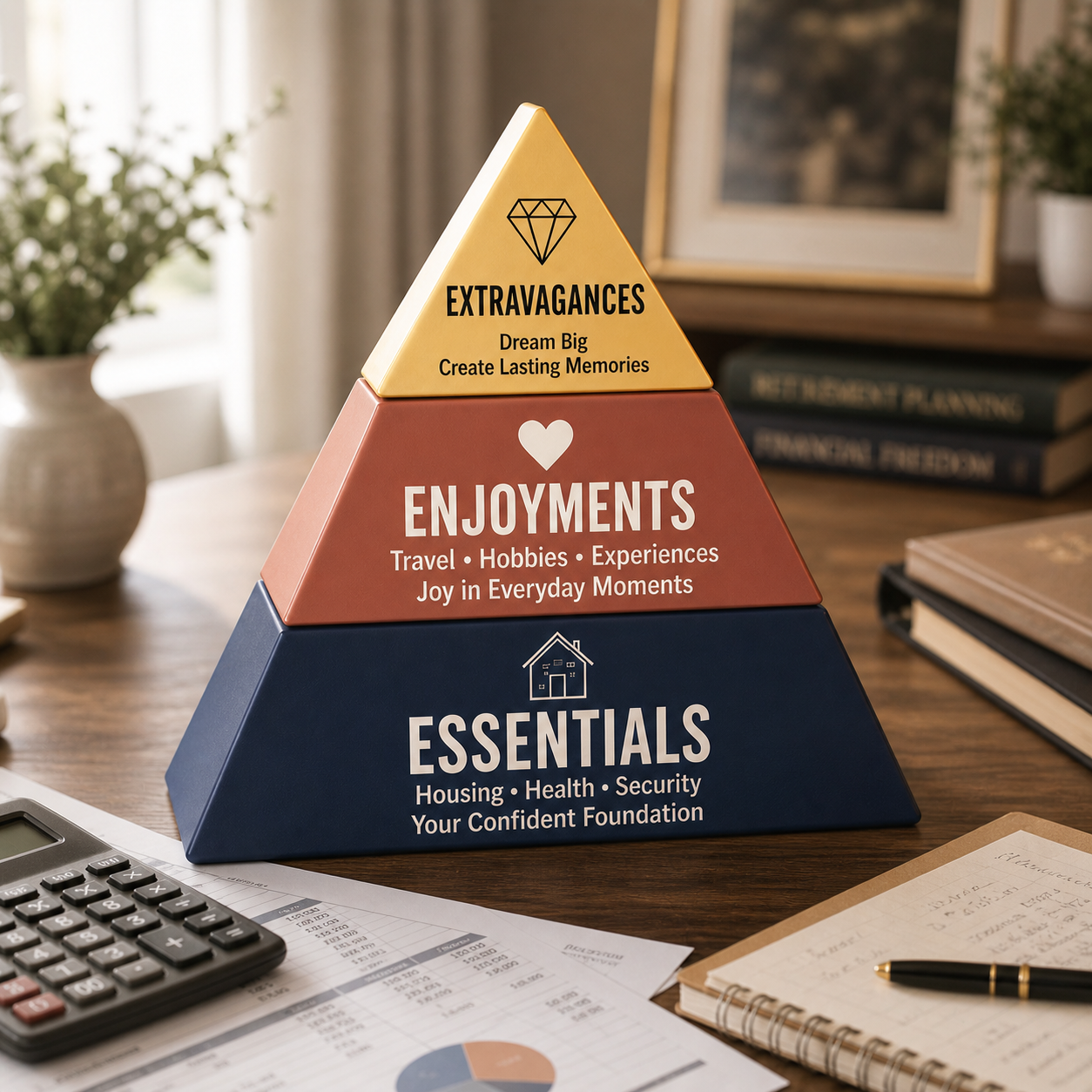

The 3E’s of Retirement

THE WISE WOMEN PROSPER FRAMEWORK

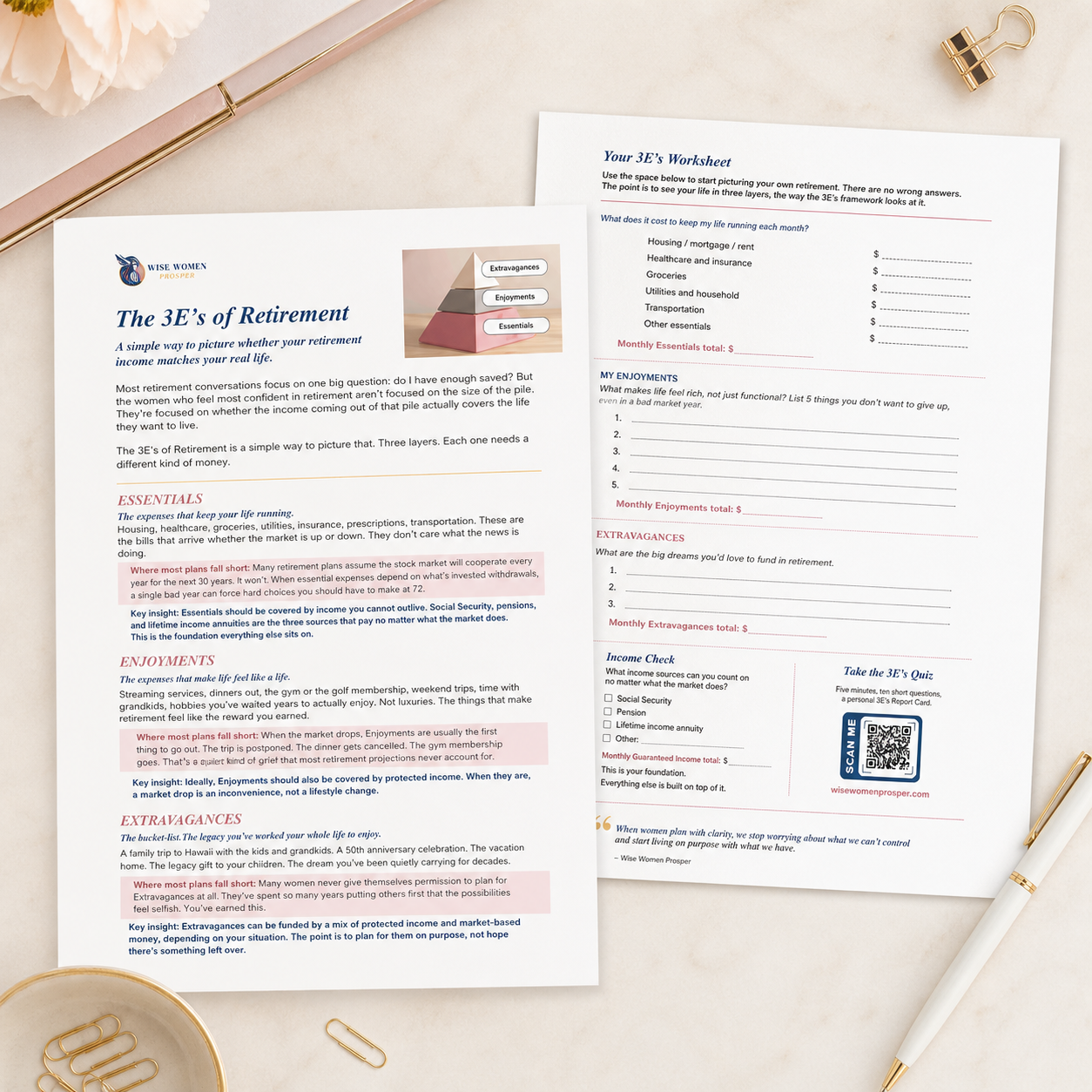

A simple way to picture whether your retirement income actually matches your real life

Most retirement conversations focus on one big question: do I have enough saved? But the women who feel most confident in retirement aren't focused on the size of the pile. They're focused on whether the income coming out of that pile actually covers the life they want to live.

Three layers. Each one matters. Each one needs a different kind of money.

That's what the 3E's framework is for.

Why most retirement plans miss the point

Most retirement plans are built around a single number. Do you have enough? The number is calculated, the spreadsheet is printed, and the woman walks out feeling either relieved or panicked depending on what the spreadsheet said.

But the spreadsheet doesn't tell her the most important thing. It doesn't tell her whether the income coming out of that money will reliably cover her life, every month, for the next 30 years.

A pile of money is not the same as income. A 7% withdrawal rate looks fine on paper until the year the market drops 25%. Suddenly the same withdrawal is taking 9% of a smaller pile, and the math that worked in the spreadsheet starts to unravel.

The 3E's framework was built to fix this. Instead of asking how much do I have, it asks what does my life actually cost, and what kind of money should pay for it?

The answer is different for each layer.

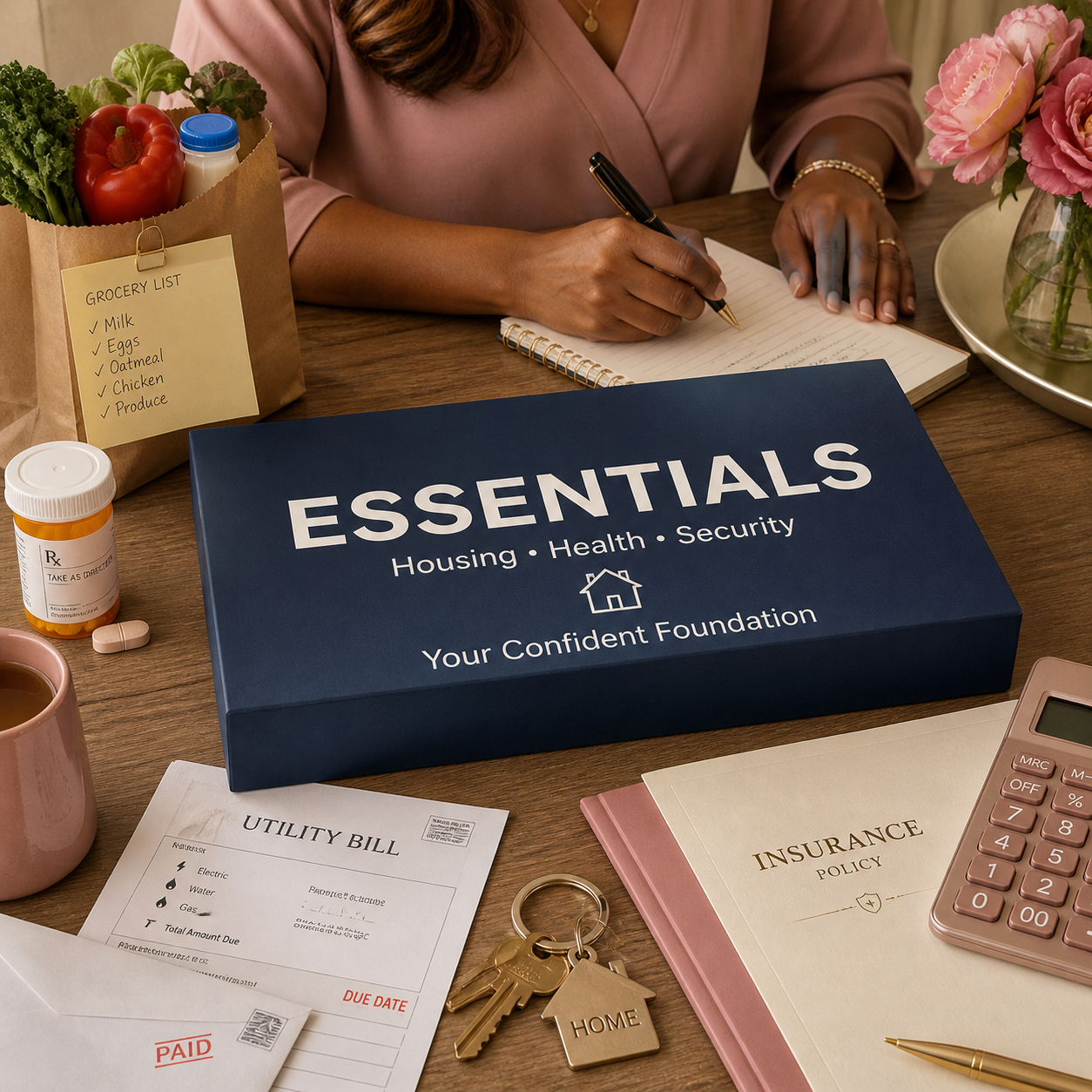

LAYER ONE | THE FOUNDATION

Essentials

The expenses that keep your life running

Housing. Healthcare. Groceries. Utilities. Insurance. Prescriptions. Transportation.

These are the bills that arrive whether the market is up or down. They don't care what the news is doing. They don't care whether your portfolio had a good year. They just need to be paid.

Where most plans fall short

Most retirement projections assume the stock market will cooperate every year for the next 30 years. It won't. When essential expenses depend on market-based withdrawals, a single bad year early in retirement can force hard choices nobody should have to make at 72.

Selling investments at a loss to pay the mortgage. Cutting back on prescriptions to make groceries work. Skipping the dentist to keep the lights on. These are the quiet retirement compromises that nobody wants to talk about, and they happen to women who did everything right.

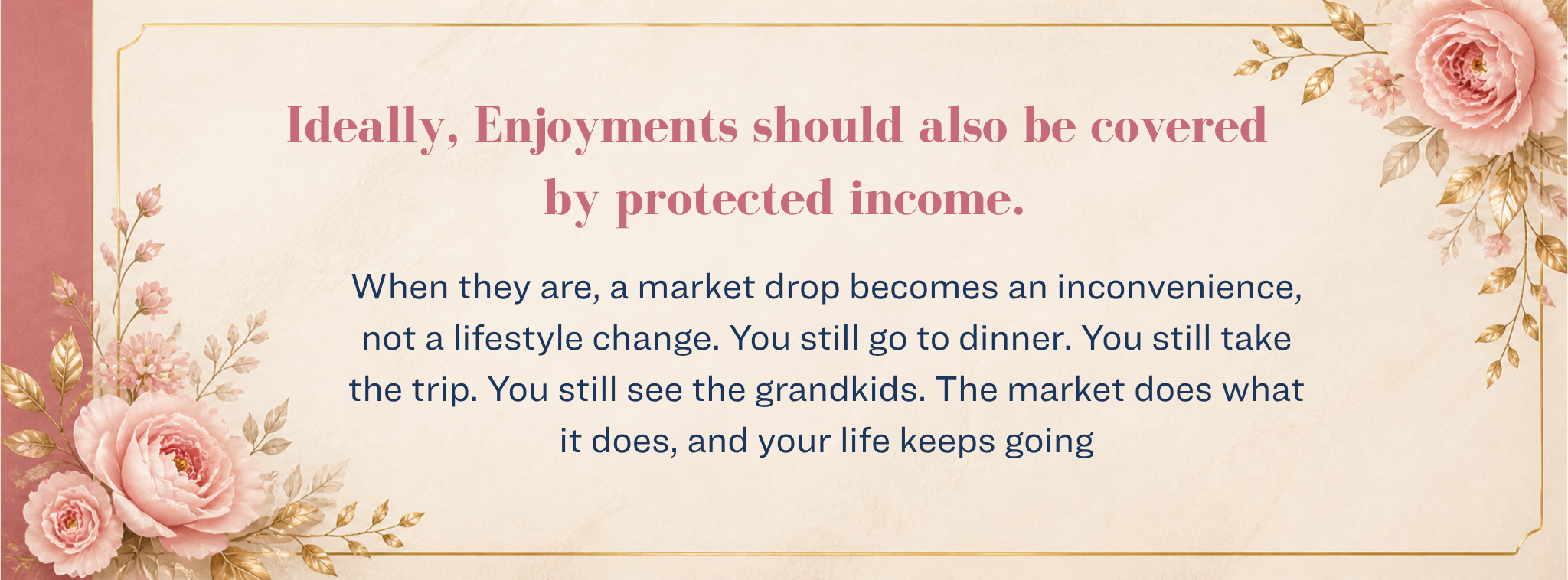

LAYER TWO | THE REWARD

Enjoyments

The expenses that make life feel like a life.

Streaming services. Dinners out. The gym membership or the golf membership. Weekend trips. Time with grandkids. Hobbies you've waited years to actually enjoy.

These are not luxuries. These are the things that make retirement feel like the reward you earned, not just the years after work ended.

Where most plans fall short

When the market drops, Enjoyments are usually the first thing to get cut. The trip is postponed. The dinner gets cancelled. The gym membership goes. The grandkids' visit gets shorter. The hobby class doesn't get renewed.

That's a quiet kind of grief most retirement projections never account for. The math says you'll be fine. The reality is that you spent a year staying home because the market scared you out of living.

A retirement that pays your bills but takes away your joy is not the retirement you saved for.

LAYER THREE | THE DREAMS

Extravagances

The bucket list. The things you've worked your whole life to enjoy.

A family trip to Hawaii with the kids and grandkids. A 50th anniversary celebration. The vacation home you've been talking about for 20 years. The legacy gift to your children. The dream you've been quietly carrying for decades.

These are the things that don't show up on a spreadsheet but show up in every late-night conversation about what retirement was supposed to be for.

Where most plans fall short

Many women never give themselves permission to plan for Extravagances at all. They've spent so many years putting others first, taking care of children, parents, spouses, and careers, that the bucket list feels selfish. Or it gets pushed to "someday." Or it becomes the thing that gets sacrificed when the spreadsheet looks tight.

It isn't selfish. You earned this. And "someday" is not a retirement plan.

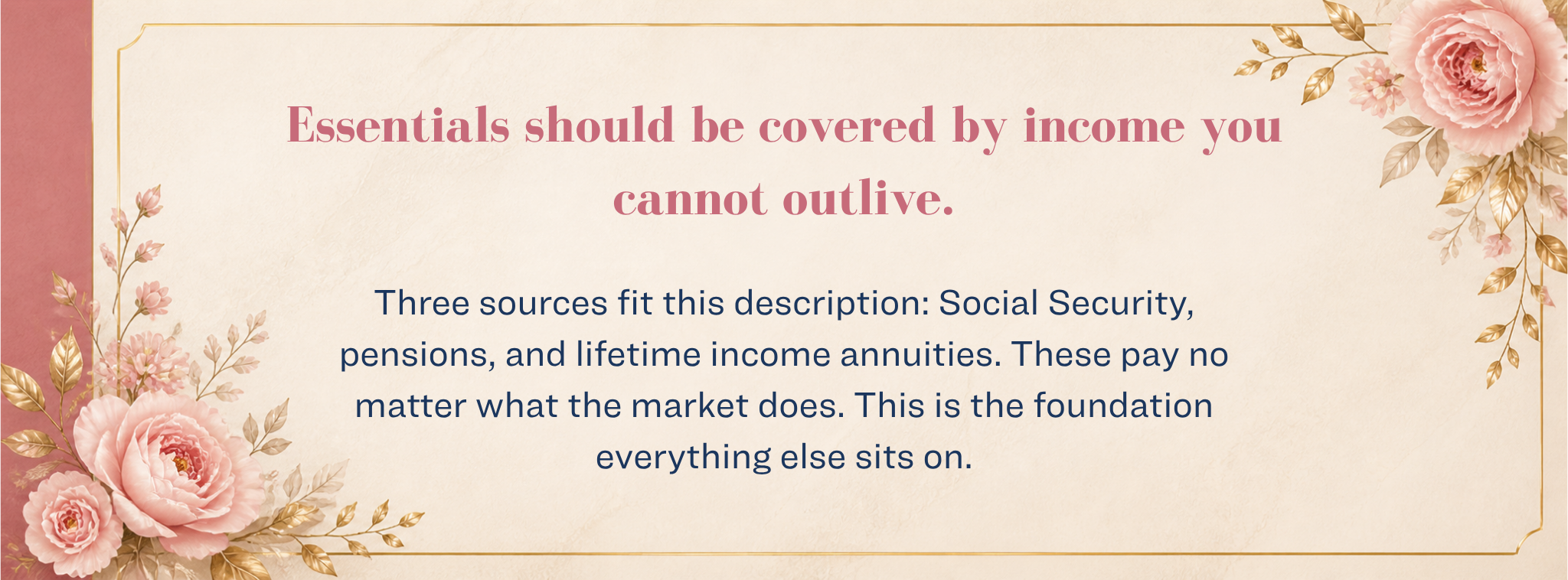

What does "protected income" actually mean?

Protected income is income you cannot outlive, that doesn't depend on what the market is doing in any given year.

There are three sources that fit this definition:

-

The most reliable income stream most American retirees have. Adjusted for inflation. Paid for life. Backed by the federal government. The single most important Social Security decision most women make is when to claim, because the difference between claiming at 62 and claiming at 70 can change a woman's monthly income by 70% or more for the rest of her life.

-

Increasingly rare, but if you have one, it belongs in the protected-income column. Most pensions pay for life. Some have survivor benefits. Some are inflation-adjusted, most are not. If you have a pension decision coming up, the choice between lump sum and lifetime payments is one of the biggest retirement decisions you'll ever make.

-

The third source. An annuity is a contract with an insurance company that, when structured for lifetime income, pays you a guaranteed amount every month for as long as you live. No matter what the market does. No matter how long you live. The guarantees are backed by the claims-paying ability of the issuing insurance company.

Different annuities are designed for different purposes. Some prioritize the highest possible monthly income. Some balance income with the ability to access principal. Some include features like inflation protection or spousal continuation. The right tool depends on what gap you're trying to fill in your 3E's picture.

Most women in retirement use a combination of all three.

The art is figuring out the right mix for your specific situation.

WHY THIS FRAMEWORK IS BUILT FOR WOMEN

Three risks women face that most plans don't account for

1. Women live longer.

The average 65-year-old woman in the United States today will live to about 87. A meaningful percentage will live well into their 90s. That means a woman's retirement income needs to last longer than a man's, often by five to seven years or more. Longevity is wonderful. It is also expensive.

2. Women are more likely to walk through retirement alone.

Roughly 80% of married men die married. Roughly 80% of married women die widowed. When a woman loses her husband, she typically loses one Social Security check, sometimes a pension, and her tax bracket compresses from married-filing-jointly to single. Her income drops at the same time her costs may be rising. Most retirement projections built for couples don't show what happens to her after.

3. Women often carried the invisible load.

Many women took time out of the workforce to raise children, care for aging parents, or support a spouse's career. That time shows up later as smaller Social Security benefits, smaller 401(k) balances, and fewer years of pension accrual. None of that is a moral failing. It's a structural reality. And it means many women arrive at retirement with the same expenses as their male peers but smaller buffers to absorb shocks.

The 3E's framework is built around these realities, not in spite of them.

A FREE TOOL FOR YOU

See your own 3E's

picture on paper

The framework becomes most useful when you apply it to your own life.

That is why we created a simple 3E’s worksheet. One page helps you map your Essentials, Enjoyments, and Extravagances. The second page helps you see what may need more attention once your three layers are clear.

Set aside about 15 minutes, print it, and fill it out honestly. Use it as a private starting point for clearer thinking, better questions, and more confident conversations about the retirement you want to protect.

3E’s of Retirement FAQ

-

No. The framework is a way of thinking about retirement income. It works whether you ever buy an annuity or not. Many women apply the 3E's lens, look at their existing income from Social Security, pensions, and savings, and find that their picture is already in good shape. Others find a gap. The framework just helps you see clearly what you have and what you might be missing.

-

The framework still applies, but Wise Women Prosper specifically serves women with $500,000 or more in retirement assets, because below that level the available solutions are different and we're not always the right fit. If you're not yet at that level, the worksheet above is still yours to use, and we can point you toward other resources if helpful.

-

No. The quiz is the fastest way to see how your current income stacks up against the 3E's framework, and it's free, but the worksheet alone will get you most of the way there if you'd rather work it out on paper first.

-

After you've taken the quiz or filled out the worksheet, the next step is a 30-minute Retirement Income Call with Veronica. It's a private conversation by Zoom, no cost, no obligation. We look at your specific picture and tell you honestly whether there's something worth doing or whether you're already in good shape.

-

This is retirement income education, focused specifically on the protected-income portion of a woman's retirement picture. We are licensed insurance professionals, not investment advisors. We do not provide investment advice, tax advice, or comprehensive financial planning. For those services, a different kind of professional is the right fit, and we'll happily refer you.

Five minutes. Ten questions. Your personal Report Card.

READY FOR THE NEXT STEP?

See where your own 3E's picture stands.

The 3E's Quiz takes five minutes. Ten short questions. At the end, you'll get a personal Report Card showing how your current retirement income stacks up against the framework, and a follow-up email walking through what your grade means.

It's the fastest way to move from understanding the framework to applying it to your own life.

Already know what you need?