FAQ Section

Frequently Asked Questions

These are the questions women ask me most often before we ever sit down together.

If you don't see yours here, the 3E's Quiz is the fastest way to get personalized answers.

About Protected Income and the 3E’s

-

Protected income is money you can count on to show up every month, no matter what the stock market is doing.

It is the income that helps cover the non-negotiables: groceries, housing, utilities, insurance, healthcare premiums, and the basic expenses that do not pause just because the economy has a bad year — or even a bad decade.

For most women, protected income usually comes from a few key sources: Social Security, a pension if you have one, and certain types of annuities designed to provide lifetime income. What these sources have in common is simple: they are not dependent on the daily ups and downs of the market.

That does not mean market-based investments are bad. They can still play an important role in retirement. But your essential expenses should not depend entirely on accounts that can rise and fall in value.

Protected income gives your retirement plan a foundation — so you can make decisions with more clarity, confidence, and peace of mind.

See if you have enough protected income for your retirement. -

A retirement account is where your money is stored.

Retirement income is the money that actually shows up to help pay for your life.

Your 401(k), IRA, or brokerage account may hold the savings you have built over many years. But those accounts can rise and fall in value, and they do not automatically create a steady monthly paycheck unless a plan is put in place.

Retirement income is different. It is the money you can count on to arrive regularly, such as Social Security, a pension, or a lifetime income annuity.

That distinction matters because retirement is not just about how much you have saved. It is about how you will turn what you have saved into dependable income you can use for groceries, housing, healthcare, travel, and the life you want to keep living.

A strong retirement plan helps turn the “pile of money” into a paycheck — so you are not left wondering, month after month, whether your savings will last.

-

The 3E's are how I help women picture whether their retirement income matches their actual life. There are three layers:

Essentials are the non-negotiables: housing, groceries, healthcare, insurance, utilities, and the basic expenses that keep your life running.Enjoyments are the things that make life feel full: dinners out, streaming services, golf, fitness, weekend trips, hobbies, and time with the people you love.

Extravagances are the bigger dreams: a special family trip, a milestone celebration, a bucket-list experience, or a meaningful legacy gift.

The reason this framework matters is that most retirement plans treat all expenses the same.

But they are not the same.

Your grocery bill is not the same as a dream vacation. Your healthcare premium is not the same as a weekend getaway. Your mortgage is not the same as a legacy gift.

That is why your Essentials should be covered first by income you can count on and cannot outlive. Your Enjoyments should ideally be supported by reliable income too, so retirement does not feel like constant restriction. Extravagances can often be planned with a mix of protected income, savings, and market-based assets, depending on your situation.

When your income is structured this way, a difficult market year does not threaten your groceries, your mortgage, or your healthcare.

That is the purpose of the 3E’s: to help you see whether your retirement income is aligned with the life you want to keep living.

-

Close, but not identical, and the distinction matters.

Protected income is a broader retirement planning concept. It refers to income sources that are designed to help cover your important expenses without depending directly on the stock market.

That may include Social Security, a pension, or certain annuities that provide lifetime income.

Guaranteed income is more specific. It usually refers to an actual promise made by a source such as the federal government, an employer pension plan, or an insurance company.

For example, Social Security is backed by the federal government. A pension is backed by the pension plan. An annuity’s guarantees are backed by the claims-paying ability of the issuing insurance company.

So, protected income and guaranteed income often overlap — but they are not exactly the same thing.

The simplest way to think about it is this:

Protected income is about the job that income does in your plan.

Guaranteed income is about who is making the promise and what that promise depends on.Either way, the goal is the same: to help create a retirement income foundation that is not left entirely at the mercy of market ups and downs.

-

Your 401(k) or IRA is an account that holds the money you have saved and invested.

Protected income is different. It is income designed to show up on a regular basis, often for life, depending on the source.

That distinction matters because an account balance is not the same thing as a paycheck.

When you retire, money in a 401(k), IRA, or brokerage account usually has to be withdrawn over time. The value of those accounts can rise and fall with the market, and you have to decide how much to take out, when to take it, and how to make it last.

That can feel especially stressful during a down market.

Most women I work with do not need to give up their 401(k) or IRA. They need to understand whether it makes sense to convert part of their savings into protected income, so the foundation of their retirement is not sitting entirely on a market roller coaster.

The rest can often stay invested for growth, flexibility, legacy planning, or larger future expenses.

That is one of the key things we look at together during a Protected Income Review: how much of your retirement should be protected, how much should stay flexible, and how to build income around the life you actually want to live.

About How Veronica Works With Clients

-

A Retirement Income Call is a 30-minute Zoom conversation.

There is no pitch, no pressure, and no sales meeting in an office.

We start with where you are right now: what you have saved, what income you already have coming in or expect to have, what your Essentials actually cost each month, and what you want retirement to look like.

Before we meet, I review your quiz answers and prepare a short slide deck to help walk you through your retirement income picture. We look at where things appear solid, where there may be gaps, and what questions are worth paying attention to next.

Everything is explained in plain English. No jargon. No overwhelm.

At the end of the 30 minutes, we decide together whether a second conversation makes sense.

Sometimes, after looking at a woman’s situation, I will tell her honestly that she may not need a second call. That happens. I would rather give you a straight answer than keep you moving through a process that does not serve you.

If a second conversation does make sense, that is when we can look more closely at specific options and how they may fit your situation.

You are never obligated to do anything.

The purpose of the first call is clarity — so you can better understand where you stand, what may need attention, and whether protected income should be part of your retirement plan.

-

No.

Both the quiz and the Retirement Income Call are no-cost, no-obligation, and no-pressure.

The quiz takes about five minutes. You answer 10 simple questions, receive your 3E’s grade, and get a personalized Retirement Income Report Card delivered to your inbox.

That’s it.

You can read it, think it over, share it with your spouse or advisor, or schedule a Protected Income Review if you would like to talk through what your results may mean.

The review is a 30-minute Zoom conversation. You learn more about your retirement income picture, and I learn more about you — what you have saved, what income you expect, what your Essentials cost, and what kind of retirement you actually want.

Nobody signs anything. There is no pressure to move forward.

At the end of the call, we decide together whether a second conversation makes sense. If it does, we can schedule it. If it does not, you still walk away with a clearer picture of where you stand.

And either way, clarity is the goal.

-

The quiz is free. The Protected Income Review is free. And there is no charge for our conversations about your situation, including follow-up calls where we may look at specific options together.

If a fixed annuity or fixed indexed annuity appears to be a good fit for your goals, I will explain how compensation works before you make any decision.

In most cases, the insurance company that issues the annuity pays me a commission. You do not write me a check for that commission, and I do not charge ongoing management fees on money held inside the annuity.

That is how these types of insurance products are commonly structured, and I believe it should be discussed openly. You deserve to understand how I am paid, what the product does, what the tradeoffs are, and how it compares to other options before you decide anything.

When we review a specific annuity, I will walk you through the details in plain English. I will explain why I believe that option may fit your situation, what problem it is designed to solve, and how it may help create the protected income you are looking for.

We may also look at more than one option together, so you can see the differences side by side — including income potential, costs or rider charges, surrender schedules, limitations, strengths, and tradeoffs.

My goal is not for you to buy “an annuity.”

My goal is to help you understand whether a specific annuity is the right fit for you.

If it is not right for your situation, I will tell you. If another option appears to serve you better, I will tell you that too. The recommendation should be based on your needs, your income goals, your comfort level, and your overall retirement picture — not on which insurance company is paying compensation.

The goal is never to pressure you into a decision.

The goal is to help you see clearly, ask better questions, and make an informed choice about whether a protected income strategy belongs in your retirement plan.

And if your situation calls for help outside my role, I will tell you that too — and point you toward the right kind of professional for that work.

-

Yes — and many of the women I work with already have an advisor.

Many financial advisors focus on managing investments and helping assets grow over time. That work can be very valuable.

Protected income planning is a different conversation.

It looks at how much of your retirement income is dependable, how much is exposed to market ups and downs, and whether part of what you have saved should be positioned to create income you can count on for life.

I do not ask you to leave your advisor. I do not manage portfolios. I do not sell investments.

My role is focused on protected income planning, including fixed annuities and fixed indexed annuities when they are appropriate for your situation.

If a protected income strategy ends up being a good fit, it can become one piece of your larger retirement picture while your advisor continues doing the work they already do for you.

And if you would like your advisor to be part of the conversation, that is perfectly fine with me.

This is not about replacing anyone.

It is about making sure you have a clear picture of how your income will support your life in retirement.

-

You’re not on your own. Not for a minute.

If you decide a fixed annuity or fixed indexed annuity is the right fit for your retirement income picture, you’ll move into what I call the Wise Women Prosper Welcome Path — a step-by-step process designed so you always know what’s next, what to do, and what I’m handling for you.

Here’s how it goes.

We start with a short funding call together — about 15 to 20 minutes by phone. We three-way in your current IRA custodian, brokerage, or retirement plan provider. When they answer, you give them permission to speak with me, but you stay in control of the call the whole way. You can pause, ask a question, or stop at any time. We request your funds be transferred over to fund your annuity.

A few days later, a bright red envelope arrives at your home from me. Inside is a simple instruction sheet, a pre-addressed prepaid envelope, and a short note. When your transfer check arrives from your current provider, you place it inside the prepaid envelope and drop it in any mailbox. You won’t have to figure out the address, the postage, or the next step.

Once your annuity is officially in force, I will be able to review an online version of your contract through the carrier’s system. These contracts are typically many pages long, so I will review the important details carefully, including the owner, annuitant, beneficiaries, premium, income features, riders, and any other pertinent sections.

Then we get on Zoom for what I call Your Settling-In Call — about 30 minutes together, side by side. I’ll help you register for online access with your carrier, log in, find your contract, statements, and account values, and confirm where everything is located on the carrier’s website. If you would like to print your contract for your records, you are certainly welcome to do so, but your contract will be available to you online.

During that call, we will also review the most important contract details together, confirm your beneficiaries are exactly as you want them, turn on electronic delivery if you prefer, and step back to talk through what your annuity was designed to do for you and how it fits the Essentials, Enjoyments, and Extravagances picture we built together.

One thing I want you to understand clearly: even though you’re working with me, you also have a direct relationship with your annuity carrier. They are the company holding your money and paying your income. You have full access to your account and your information through them, anytime. I’m your guide and your advocate, but the contract is between you and the carrier, and you should always be able to see and reach your money.

Annuity guarantees are subject to the claims-paying ability of the issuing carrier.

-

I currently serve women in Arizona, California, and North Carolina.

I work as a virtual advisor, so our appointments are always held by Zoom. There is no office meeting, no pressure, and no need to drive anywhere. We simply meet online and talk through your retirement income picture together in plain English.

If you live in another state, you are still welcome to take the 3E’s Quiz and read the educational content on this site. The concepts can be helpful no matter where you live.

However, I am only licensed to make specific insurance product recommendations or place business in Arizona, California, and North Carolina.

If you are close to a state line, split your time between states, or are planning to move, we can talk through what that may mean for your situation.

About Annuities Specifically (the Elephant in the Room)

-

Some are. Some aren't. The category is too broad to label all of it good or bad, and the women who tell me "I heard annuities are bad" usually heard it about a specific kind of annuity that I don't sell.

The criticism is often aimed at variable annuities, which are a different product class entirely. Variable annuities put your money in subaccounts that rise and fall with the market, often come with high internal fees, and have a long history of being oversold to people who didn't understand what they were buying. The criticism of variable annuities is largely deserved. I don't sell them.

There has also been legitimate criticism of certain indexed annuity products that were sold with overly complicated structures, hidden fees, or unrealistic illustrations. That criticism is fair too. The fixed and fixed indexed annuities I work with are simpler products with transparent structures, principal protection, and clear lifetime income mechanics. They're not the right fit for everyone, and I'll tell you when they're not. But they're not the products the headlines were written about.

The real question isn't "are annuities good or bad." It's "is this specific annuity, with this specific carrier, the right tool for this specific part of my retirement plan." That's the conversation we have together.

-

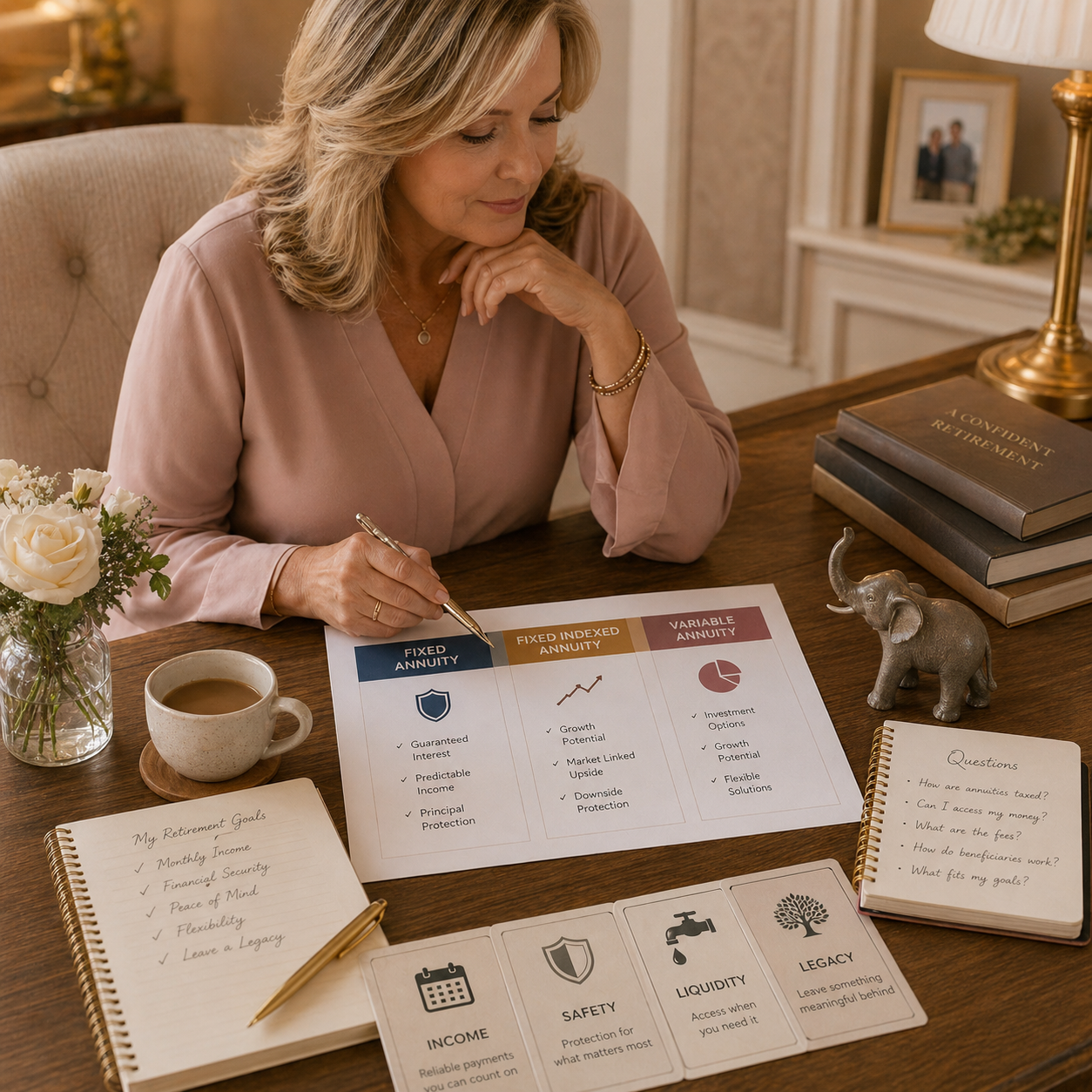

These three products share a name and almost nothing else. Here is the simple version:

A fixed annuity is designed to provide safety and predictability. You place money with an insurance company, and the company credits a stated interest rate for a set period of time. Your principal is protected from market losses, and the growth is generally modest and predictable.

Some people compare this to a CD because of the fixed interest concept, but there is an important difference: annuities are not FDIC insured. They are backed by the claims-paying ability of the issuing insurance company.

A fixed indexed annuity also protects your principal from market losses, but the interest you may earn is linked to the performance of an index, such as the S&P 500. You are not directly invested in the market. Instead, the insurance company uses a formula to determine how much interest is credited.

That formula may include things like caps, participation rates, or spreads. In a strong market year, you may receive some of the upside. In a down market year, your principal is not reduced by market losses, although surrender charges may apply if you take out more than allowed during the surrender period.

Fixed indexed annuities are often used by people who want some growth potential, but do not want their retirement income foundation exposed directly to market losses.

A variable annuity is different. With a variable annuity, your money is typically invested in subaccounts that can rise and fall with the market. These products can involve market risk, internal fees, and more complexity. They also require a securities license to sell.

I do not sell variable annuities, so they are not part of the protected income planning work we would do together.

The most important thing to understand is that not all annuities are the same.

A fixed annuity, a fixed indexed annuity, and a variable annuity may share a name, but they behave very differently.

So the real question is not, “Are annuities good or bad?”

The better question is:

“What kind of annuity is this, how does it work, what are the tradeoffs, and does it fit the job we need it to do in your retirement plan?”

-

If a fixed annuity or fixed indexed annuity is placed, I am paid a commission by the insurance company that issues the annuity.

You do not write me a check for that commission, and I do not charge ongoing management fees on money held inside the annuity.

That is how these types of insurance products are commonly structured, and I believe it should be discussed clearly and up front. You deserve to understand how I am compensated, what the product does, what it does not do, and what costs or limitations may exist before you make any decision.

When we look at a specific annuity together, I will walk you through the details in plain English, including why I believe it may fit your situation, how it compares with other options, what problem it is designed to solve, and what tradeoffs come with it.

We may also look at more than one option side by side, so you can see the differences for yourself.

If you are wondering whether compensation creates a conflict of interest, that is a fair question — and I respect you for asking it.

The honest answer is that I am paid when business is placed. That is true for many professionals who work with insurance products. But my responsibility is to help you understand whether a specific annuity is appropriate for your needs, your income goals, your comfort level, and your overall retirement picture.

I will not recommend an annuity simply because compensation is available.

If an annuity is not the right fit, I will tell you. If another option appears to serve you better, I will tell you that too.

My goal is for you to make an informed decision with clarity, confidence, and no surprises.

-

Not from market losses.

With a fixed annuity or fixed indexed annuity, your principal value is not reduced because the stock market has a bad year. If the market drops, your annuity value does not drop with it due to market performance.

That is one of the main reasons these products are used in protected income planning.

However, that does not mean there are no rules, limits, or tradeoffs.

There are situations where the amount you walk away with could be less than expected.

The first is if you take out more than the contract allows during the surrender charge period. Most annuities have a surrender period during the first several years of the contract. During that time, the insurance company may charge a fee if you withdraw more than the free withdrawal amount allowed each year.

The second is if withdrawals are taken in a way that affects the remaining account value or any income benefits attached to the contract. Taking too much, too soon, can reduce what is available later.

That is why we look closely at the details before you ever make a decision.

We will walk through the surrender schedule, the free withdrawal rules, any income rider provisions, and what happens if you need access to more than the contract allows.

The goal is for you to understand exactly how the annuity works — not just the benefits, but also the limits — so you can decide whether it truly fits your retirement income plan.

-

In most fixed and fixed indexed annuities, any remaining account value typically passes to the beneficiaries you have named on the contract.

That is one of the features that often surprises people. An annuity is not simply “gone” when you pass away. The details depend on the specific contract, but your beneficiaries may have options for how they receive the remaining value, such as a lump sum or payments over time.

Naming beneficiaries directly on the annuity contract can also help make the transfer more direct for your family, often without going through probate. Of course, estate and tax rules can vary, so it is always wise to coordinate beneficiary decisions with your legal or tax professional.

If you have selected a lifetime income option, the rules can vary depending on how the contract is structured. For example, it may depend on whether the income is based on one life or two, whether income has already started, and what riders or features are attached to the contract.

That is why we do not guess.

We walk through your specific contract together so you understand what happens in different scenarios — while you are living, if income has started, if income has not started, and what your beneficiaries may receive when you pass away.

This is also why we carefully review beneficiary designations during the process. It is one of the most important parts of the contract, and one of the easiest details to overlook.

The goal is simple: you should understand how the annuity supports your income while you are here, and how any remaining value may pass to the people you care about when you are gone.

-

Yes — but there is structure around how access works.

Most fixed annuities and fixed indexed annuities include a free withdrawal provision, which allows you to take out a certain percentage of your account value each year without a surrender charge. A 10% annual free withdrawal is common, but the exact amount depends on the contract.

That means some money is available to you each year, for any reason, without a surrender charge from the insurance company.

If you withdraw more than the free withdrawal amount during the early years of the contract, surrender charges may apply. These charges typically decline over time and eventually go away, often after 5 to 10 years, depending on the product.

After the surrender period ends, you typically have access to your money without surrender charges.

Some contracts also include provisions that may waive surrender charges in specific situations, such as a terminal illness diagnosis or certain long-term care needs. These provisions vary by insurance company and product, so we would review the exact details together before you make any decision.

The honest reality is this:

An annuity is designed for income and protection. It is not meant to be your emergency fund.

That is why we never put money into an annuity that you might need access to in the next few years. Your liquid savings should stay liquid. Your annuity money should be the part of your savings you have already decided is for the long haul.

The goal is to create protected income without sacrificing the flexibility you still need in the rest of your retirement plan.

Reach out anytime. Whether you have a question, want to learn more about an upcoming workshop, or are wondering whether protected income planning makes sense for your situation, we're here to talk it through.

Give us a call at 928-582-7661 or fill out the form here. We'll respond as quickly as we can, usually within one business day.

If you're ready to take a closer look at your own retirement income picture, the fastest place to start is the 3E's Quiz. It takes about five minutes and gives you a clearer sense of where you stand before we ever talk.

You Are Invited to Connect With Us!